Managing Credit Card Debt

SHARE THIS GUIDE

You keep deleting those ‘payment due reminder’ emails, so do 3 million people in the UK. Or so we’re assuming since that whopper of a number represents those who can't afford to pay off their credit card bill. Unlike in politics, this is one majority you don’t want to be a part of, trust us! And you’ll feel so much freer when you’re not.

Mo credit, mo problems

It's way too easy to spend on a credit card and think about it later. Case in point: How many times have you bought a round of drinks or splurged on ‘I-know-I-shouldn’t-buy-them’ shoes using the magic ‘free money’ card? We thought so. So step away from the card, lock it up and only use your ‘real-money’ card (that's your debit card) from NOW on.

Magic card gone…what’s next?

It’s time to chip away at that debt. First things first – find out where your money is going. There’s a MOXI guide for that: A Personal Budget That Works For Me shows you how to track your spending and identify the black holes in your bank account.

But how does this help me with debt?

When you know where your money is going you can work out your ‘rescue fund’. This is how much you have leftover each month to pay off your debt. Zero, zip, nada in the pot? If your rescue fund is non-existent it’s time to knuckle down, squeeze those big spends and not treat yourself for a while. As depressing as that sounds, the feeling of freedom from debt will be so worth it in the end.

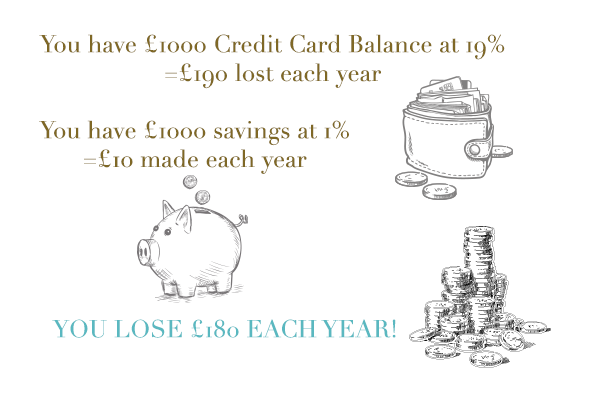

I have savings, should I use them to pay off my credit cards?

100%. Saving and having credit card debt simply doesn’t make sense because you pay more interest on your credit card than you make from your savings.

Talk me through the payment process

Make a list of all your cards and the interest you pay on each. Those with the highest interest should top the list. Get rid of these first because they’re costing you the most.

Anything else I need to know?

Credit card companies are competing for your debt. True story. They want you to pay them interest instead of your original credit card provider. Their tactics usually involve offering an interest-free period on balance transfers (this is when you move the total amount you owe on a credit card to a different card). Browse interest free cards here.

So should I consider a balance transfer?

Definitely. Every month you’re losing money to interest and the longer it takes you to pay off the more you lose. If you transfer your balance to an interest-free card it buys you time. Be warned – this doesn’t mean you should ignore payments (or delete payment reminder emails for that matter). Instead make it a point to pay as much down as you can while you’re not accumulating more debt on interest.

And there’s no catch?

Not exactly. Before you transfer everything over to a new card take stock of these two points:

1. You'll have to pay a Transfer Fee. Normally it’s a charge of around 3% of your balance. This is so the new company can collect some profit when you join in case you’re smart enough to pay off all your balance in the free interest period. Despite this fee, it’s still a good deal as long as you get a minimum of three months’ interest free.

2. Note the interest rate. This is what will kick in once the free period is over. If you’re unable to pay off the balance in the 'free' months, you don’t want to be paying more interest than you are today.

When applying for a new card the above will be made crystal clear. Those are the rules.

Category

Tags

Budgeting, Credit Card, Current Accounts, Debt, Interest, Savings ,