How To Manage Your Pension

SHARE THIS GUIDE

We know, you’re paying into your pension and already dreaming of Caribbean cruises come 55. Now what? Well, to start, if you want to make island cruising a reality (or more realistically, simply be comfortable in your retirement) it’s important you know some key facts to get the most from your pension.

Okay, I’m listening

Money put into a pension is invested. Where? Usually in funds which are made up of investments in large companies. There are different ways to invest in companies - it could be through buying shares or lending them money - we have a guide for that.

Er, what is a fund?

A fund pools together money from lots of people and a fund manager decides how to invest this money. The fund will usually be made of different products called assets.

I’m still not sure what exactly a fund is…

Funds are made up of different types of investments (aka assets) and the risk level of the fund depends on what assets are included. From lowest to highest risk, here are the assets you may see:

Cash… a short-term loan in return for interest.

Bonds… money lent to a company or government in return for interest.

Property… buying mass commercial or residential properties.

Shares… buying a piece of a company (aka equities).

Commodities… buying gold, coffee, oil and anything else tangible.

Workplace vs Personal Pension? Help!

If you’re offered a workplace pension where your employer also contributes you’d be silly not to take it because it’s free money. And, if your employer does not offer a pension today they'll have to in 2018 under new government rules. You’re also allowed to open a personal pension in addition to your work pension. Self-employed or a freelancer? Sorry folks, your only option is the personal route.

That’s easy enough. But how do I set up my pension?

If you’ve got a workplace pension your employer chooses the pension provider, this provider may offer you a choice of funds. If you do not choose a fund your money will go into a “default fund”. You should be given all the details and may have an online login to monitor how it's performing. If you don’t know what other funds are on offer find the person in the company responsible for pensions and ask - it’s within your rights!

For personal pensions, you have more choice. You’re a free agent so shop around. You don’t have to be tied to one provider and your investment choices will be wider. Finance newbies, fear not! We have a guide for this.

You lost me at Default Fund

This is the financial equivalent of a Funds for Dummies manual. The employer selects this fund for all their employees who do not have the financial know-how or assistance to choose their own. Sticking to this default fund might be easy and convenient but it’s likely not the best performing fund. Still, a whopping 4 out of 5 people use them (what’s up with that?).

Okay, I’m sold. I want to choose the fund

You may have access to lots of different funds through your pension provider and, once your pension pot is sizable, you can select more than one fund to diversify your investment. This means you’ll likely get more bang for your buck. Swot up on 5 Steps to choosing a fund for tips.

How do I know a fund is ‘good’?

Every fund comes with a factsheet which includes a past performance chart and future targets. A medium-risk fund could aim to return 4.5% a year. So if you were to deposit £300 per month into your pension for 30 years and the fund returns 4.5% a year on average you’ll end-up with a pot worth £196,000 by retirement (this assumes a 0.75% annual fund charge)

What are my options?

You can see what investments are being made by the fund and, if you don’t like the companies receiving your £££'s, you can choose a more suitable fund. You can also opt to invest in a fund that has the potential to bring higher returns or you may want to play-it-safe and select a lower risk fund.

High returns. Low risk. What??

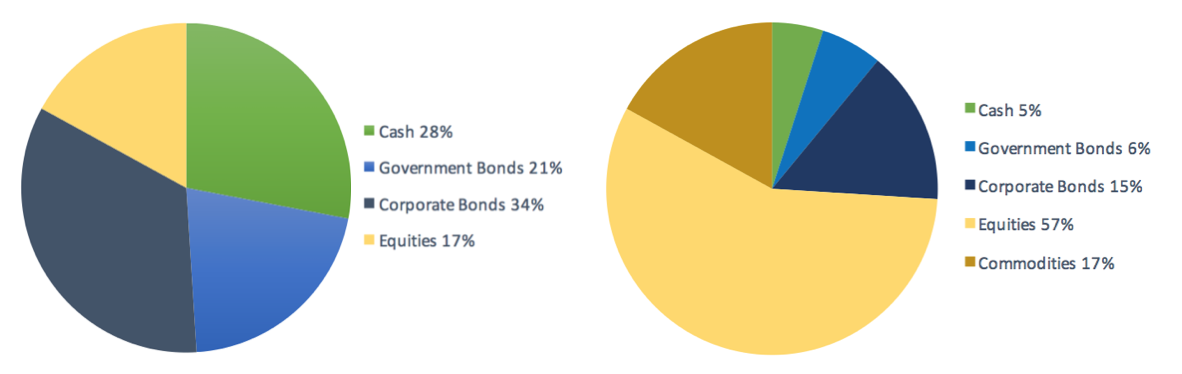

Here’s the schtick: Higher risk funds are more likely to move up and down because they’re made up of products with more volatile prices. Commodities and equities (aka shares in a company) are considered to be the most volatile investments and funds with a larger portion of these are labelled as 'higher risk'. Low-risk funds are made up of a larger portion of bonds and cash investments.

The below illustrates the difference in investments (aka assets) between a low risk and a high risk fund. You'll find a similar illustration labelled 'Asset Allocation' in your Fund's Factsheet.

Low Risk vs High Risk

I just fell asleep. Tell me in real terms.

Yeah, we know it’s boring so here’s the gig. The point of having a pension is to create an income in retirement and as you get closer to this age you’ll want to protect your capital. However, in the early years you may want to try grow your capital using a medium or higher-risk fund and when retirement is approaching switch to a lower-risk fund to limit the chances of a stock-market crash shrinking your pot just before you need it!

Are there fees involved?

Unfortunately, understanding all the fees is not straightforward so we created a guide for that – Your Crib Sheet to Pension Fees.

What else should I know?

If you have a workplace pension your employer usually matches contributions up to a certain amount. This is free money which you should take advantage of and it’s wise to top-up your pension within your means, better to act now than scramble for money later. As you earn more and get closer to retirement make the most of this huge tax saving by ditching more dough into your pension pot.

MOXI round-up

At least once a year, check-in on your pension to see how it’s performing. Most providers have an online login where you can access this information but whatever the case the pension provider should send you an annual statement showing how much the fund has grown in value (and hence how much your money has grown), your balance, the fees and a projection of what you will have at retirement.

Category

Tags

Asset Allocation, Assets, Fund Factsheet, Funds, Pension Default Fund, Pension Provider Fee, Pension Providers, Personal Pension, Workplace Pension ,