Guide to Funds

SHARE THIS GUIDE

A golden rule in the investment world is to spread your money around aka diversify. It's a seriously good way to reduce your risk. But, choosing different companies to invest in can be a tedious task. Enter funds. With one investment your money is spread across many different companies, industries and even countries. It’s almost too good to be true (but trust us, it is).

In this guide:

- What is a fund?

- The fees

- What investments are included in a fund?

- How do funds make you money?

- Paying tax on funds

Backup please. What exactly is a fund?

It’s a goodie bag of investments which have been purchased using a pool of money from hundreds or thousands of people. That means thousands of people can be the owners of a fund. The Fund Manager makes the day-to-day decisions on what investments are made.

Why should it be on my radar?

Because you’re likely already using one. Nearly all pension schemes invest into funds so even if you’re not shopping for a fund now, you’ve already paid into one as part of your long term investment plan (hurrah!). They can also be a great way to invest past your pension and, unlike your retirement fund, you can access it before you are 55.

Tell me again why they’re so great

It’s an easy, instant way to spread out your investments and means you don’t have to make a lot of decisions. Even better? After you decide which fund to invest in, the fund manager will do the work for you (score!). Your job is to check in every so often to see how your fund is performing. Easy peasy.

Any cons?

As with anything that makes life simpler, you have to pay for the convenience. The fund charges a yearly fee known as Ongoing Charges Figure (OCF) or Total Expense Ratio (TER). This pays for the Fund Manager’s expenses and expertise for providing the service. It is charged as a percentage of your total investment, ranging from 0.1% to 2% a year - that is, £10 to £200 for every £10,000 invested.

Your broker charges an annual fee as well. Whilst the broker is not managing your money they are providing you with a platform and all the administration that comes with it. The fee is a percentage of your investment but, unlike the OCF fee, it is usually capped. You can find a list of broker fees here.

Side note: Other fees to look out for are one-off fees such as entrance (or initial) and exit or switching fees. These should all be made very clear on the fund’s information page.

So how do I actually invest in a fund?

Funds are available online from a number of places including your bank or stock broker. Each fund has a unit price and you can decide how many units you want to buy. For example, say the fund ‘The UK’s Top Businesses’ costs 130p a unit (or £1.30) and you buy 1,000 units, your total investment size is £1,300.

Your online broker account will share loads of information about each fund to help you make your choice. It’s easy to set up, deposit and invest in a fund – we swear! To avoid paying tax on your profits you can open a Stocks & Shares ISA and buy into a fund through that account.

Do I need a lot of £££ to invest in a fund?

Not at all. Some funds allow you to start with as little as £100 and you can choose to add to this each month. You should be prepared to invest for a minimum of five years because if a fund experiences a bad year or two you may need time to ride it out.

What should I look for when choosing a fund?

There are a number of things to consider. You’ll need to go through a checklist to decide. We have a guide for this.

How much money can I make?

A medium-risk fund may aim to return 5% a year on average. Meaning, if you invest £10,000 and keep the yearly profit in the fund your investment will be worth £12,800 after five years and £16,300 after ten years. Note: This hasn't deducted any fees so you’ll actually take home less.

What investments are included in a fund?

Every fund is different and is made up of different investment products. These products - known as assets btw - starting from lowest risk, are:

Cash… money deposited in bank accounts or used in short-term loans in return for interest payments.

Bonds… money lent to large companies or the government in return for interest payments.

Property… the pounds used to buy commercial or residential property.

Stocks and shares (aka equities)… money used to buy portions of different companies.

Commodities… this can be gold, oil, coffee beans, and anything else tangible.

Depending on the combination of products used, the fund can be labelled as low, medium or high risk.

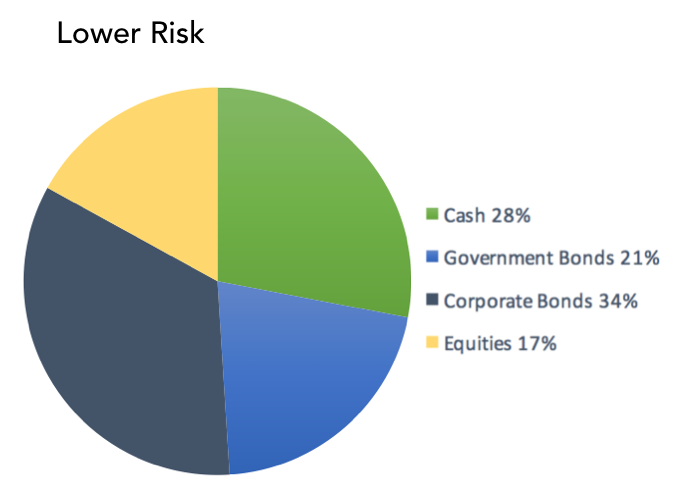

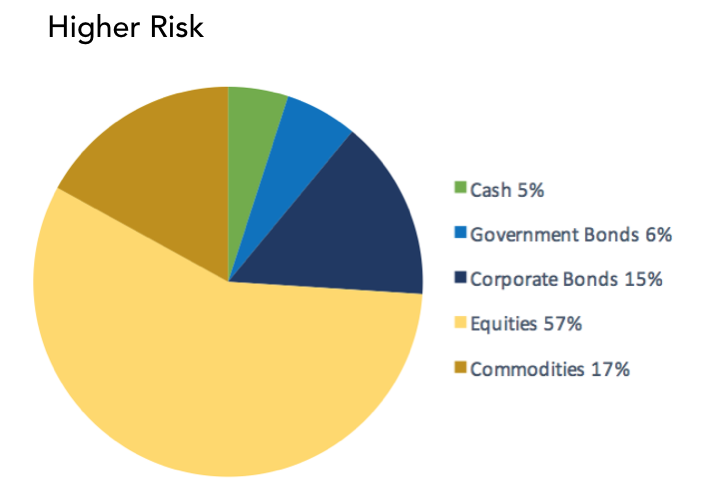

MOXI Tip: Funds that contain mainly cash or bonds are lower risk while those with more equities or commodities are higher risk.

The below pie chart (we love these!) illustrates a low-risk fund vs a high-risk fund. The choice of assets included in a fund is known as 'Asset Allocation' and is always shown on a Fund's Factsheet.

How do funds make you money?

We know, we know, this is what you really want to know so let’s get down to business. The way money is made depends on the investment. So if you own bonds or make a short-term loan you receive interest. If you own shares you receive dividend payments (a slice of the company’s yearly profit). If you own something and it goes up in value (like share or a house for instance) you can make a capital gain.

Need a refresher? Read our investment guide.

So what does a fund pay?

A fund is made up of different investments so it makes money in all these different ways - interest, dividends and capital gains.

Got it. But how do I get paid?

A fund invests in many different things and places. The interest and dividends from these investments are paid out regularly. It's the fund’s duty to pass this income on to you and all the other owners of the fund.

If you own an Income Fund this income is deposited directly into your bank or broker account. If you own an Accumulation Fund, this income is kept in the fund and reinvested.

Which is best?

Well, while it’s nice to receive a little money every now and again, reinvestment does stop you from spending it right away (yawn) since it keeps the money locked up in an investment. But it’s your choice if you want regular income now or prefer to keep it for the future.

What about capital gains?

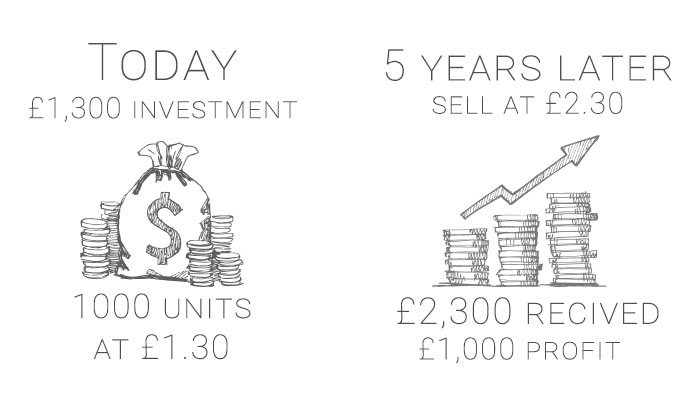

Similar to investing in individual shares, a fund can go up in value. This may happen if the fund invests in bonds, companies, property or commodities that have been successful and gone up in price. If you sell your units in a fund that has gone up in value, you’ll make a capital gain.

For example, if you bought 1000 units at £1.30 today (a £1,300 investment) and in five years sell them all at £2.30, you will receive £2,300 which is £1,000 profit (high five all around!).

Paying tax on funds

So here’s where funds get complicated. They can make you money in three ways: Through interest, dividends and capital gains. And yes, there are different tax rules for each. Pens at the ready!

The three ways to make money

Interest income is tax-free up to your personal saving allowance (PSA), which is £1,000 for basic-rate tax payers and £500 for higher-rate tax payers. Any interest earned above this will be taxed in the same way as your salary. Not sure where you sit on the income tax pay scale? Find out here.

Dividend income is tax-free up to £5,000 a year. Any dividends earned above this will be taxed depending on your total yearly income (from salary and any other taxable earnings you receive), here are the bands…

| Your income tax band | Tax rate on dividends over £5,000 |

| Basic Rate (earning £11,501 to £45,000) | 7.5% |

| Higher Rate (earning £45,001 to £150,000) | 32.5% |

| Additional Rate (earning over £150,000) | 38.1% |

What counts as taxable income? We have a guide for that.

Capital gains made when you sell your fund is tax-free up to £11,300 a year. Any capital gain above this will also be taxed depending on your income band.

| Your income band | Tax rate on capital gains over £11,300 |

| Basic Rate (earning £11,501 to £45,000) | 10% |

| Higher Rate (earning £45,001 to £150,000) | 20% |

| Additional Rate (earning over £150,000) | 20% |

MOXI top tip: Capital gains tax is applied to many things – funds, shares, jewellery, second homes. To check you’re within your tax-free allowance, you’ll need to add up all your capital gains.

How do I work out if and when I owe taxes?

Interest and dividends payments are paid to you regularly (usually twice a year) and, if over your allowance, you have to pay tax on these in the same year. You’ll only pay capital gains tax at the time of selling the fund.

Tax on Interest and Dividends

Your fund’s annual statement will break down the interest and dividend income you receive so check these against your tax free allowances. If you’re within the allowance, congrats, you’ve got nothing to do. Sit back, relax and pop on the Kardashians (no judgement). If you’re above, well, you’ll need to handover some of your income to HMRC (you can still watch Kim and Kanye, natch).

MOXI top tip: Keep your annual statements in a safe place because you may need them if your taxes are ever reviewed. If they’re sent by post, take a photo and email them to yourself.

Tax on Capital Gains

Some good news: You only need to work out your capital gain if you’re selling the fund. Plus, you only pay tax on any ‘gain’ over £11,300. The gain is the difference between the price you bought and the price you sell the fund at. So say you buy 10,000 units in a fund at £1 - which is a £10,000 investment - and years later sell at £5 per unit, you’ll receive £50,000. Your gain? That’s £40,000 (£50,000 return minus £10,000 initial investment). You can deduct any broker fees, say £1,000, from this as well as your tax-free allowance, £11,300. Now you’re at £27,700 which will be taxed as a capital gain. For a higher-rate tax payer this is a bill of £5,500. We feel your pain.

Is there any way to avoid paying tax on funds?

Well, if there’s a good chance you’ll go over your tax-free allowances you might want to open a Stocks & Shares ISA which protects your investment income from being taxed. BUT this limits you to investing £20,000 each tax year (from April 6th to April 5th the following year).